… or potentially, the key to put your mind at rest

For those of you with international profiles – living abroad, or who own assets abroad – new EU measures represent a major step forward for your estate planning.

And this will apply from August 17th, 2015.

Under current French inheritance law

French inheritance laws are very different from those of the United Kingdom.

In France you are not free to dispose of your whole estate as you may wish.

Upon death the deceased’s estate is divided into two sections, called:

- « la réserve héréditaire », or what’s known as « forced heirship »– which must be left to any protected heirs, i.e your children

- and « la quotité disponible », which represents the free part of your estate, which can be left to whoever you wish.

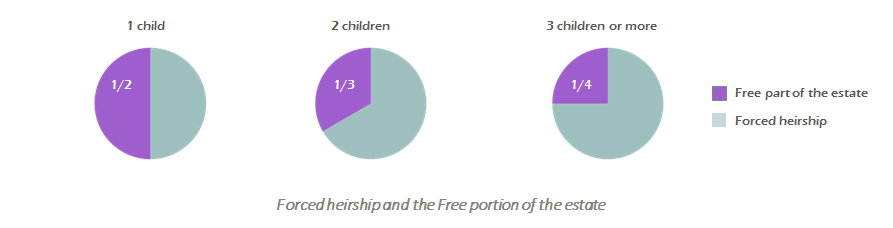

If you have children, and whether you draft a will or not, you cannot disinherit your children. They are legally entitled to a share in your estate:

- If you leave 1 child, he/she is entitled to 1/2 of the estate,

- If you leave 2 children, they are entitled to 1/3 of the estate each,

- If you leave 3 or more children they are entitled to 3/4 of the estate in equal shares.

You may have already taken measures to mitigate French inheritance rules, you may have:

- changed your marital regime,

- created an SCI,

- bought in tontine,

- put in place a gift between spouses, etc.

Whether you have taken measures or not, your situation will need to be reviewed in light of the new EU regulation.

« Forced heirship » rules will not disappear, but from August 2015 it will be possible for some of you to dispose freely of your whole estate.

New inheritance rules under EU regulation n°650/2012

From August 17th 2015:

- If the deceased says nothing in his/her will, or in the absence of a Will, his/her last habitual residence at the time of death will determine the laws of his/her succession.

- However, the testator is allowed to designate his/her national law (at the time of the choice or the time of death) as the law governing his/her succession as a whole, by stating his/her choice expressly and in testamentary form.

For example an English citizen can choose English law to govern his/her succession as a whole, by stating so in a will.

The context of these rules

The purpose of Brussels IV is to facilitate free movement, within the EU, by removing the obstacles faced by EU citizens in asserting their rights in the context where the deceased’s assets are situated in different countries.

In particular it provides certainty as to which law will apply in governing your succession.

The regulation is of universal application

Whether it be the law of the country of habitual residence or the law of the testator’s nationality, said law will govern the succession as a whole, including all worldwide assets, regardless of their nature (movable or immovable assets), and their location (whether they are located in another EU State or a state outside the EU).

When does it come into effect?

The regulation:

- came into effect on August 16th 2012,

- but will only apply from August 17th 2015.

In practice this means that you can already prepare your inheritance in accordance to said regulation, by writing your will now, however it will only apply if you live until August 17th 2015.

What can this mean for you?

It will facilitate your estate planning

Because not only will you be able to choose the law applicable to your inheritance; but said law will govern the whole of your worldwide assets.

It will enable you to mitigate side effects of the law of habitual residence

If the law of your habitual residence doesn’t permit you to dispose of your estate how you wish, you may choose your national law to achieve your aim.

For example if you are an English national living in France, you can choose English law and therefore avoid the French « forced heirship » rules, enabling you to dispose freely of your entire estate.

Exit some old strategies, like creating an SCI to avoid French inheritance rules. A simple Will may suffice.

A sole and unique law governing the whole of your succession will simplify international inheritances considerably.

However every clients situation is different and needs careful analysis and even though these new rules will open up great new perspectives, their application will not be plain sailing – seek the best advice to protect the ones you love, and put your mind at rest.

Some foreseeable difficulties

The UK, Ireland and Denmark have opted-out of EU Regulation n°650/2012

In practice this will have a strange effect:

- UK citizens living abroad will be able to benefit from these rules,

- Whereas other EU citizens (French nationals, for example) living in the UK will not, because the UK does not abide by the regulation.

So if said French national, living in the UK has property in the UK, he cannot chose for said property to be dealt with under French law.

The concept of Habitual residence adopted by the EU has not been defined

It may reveal difficult to prove; and the lack of definition leaves room for manipulation.

If we take the example of the UK, UK’s internal private law is coordinated around the concept of « domicile ».

Said notion is complex and involves numerous aspects, encompassing habitual residence, place of birth and centre of economic interests, etc…

In English law an English national may have lived a large part of his life outside of the United Kingdom and still be regarded as « domiciled’ in his country of origin if he/she intends to return.

In practice, we may be confronted with situations whereas:

- An English lawyer will consider the deceased domiciled in England and apply English law, and a French notary who will consider the deceased to have his habitual residence in France, and apply French law to the whole of the deceased’s estate.

Therefore it is essential to explicitly choose the law that will govern your future inheritance in a will.

- Acceptance and application of EU Regulation in a third member State

- Other issues concern the domains excluded by the Regulation, such as:

- Matrimonial regimes…

- Gifts …

- Tax issues

These will remain governed by the state in which the assets are held and double tax treaties between the states is they exist.

Because of the disparities in « tax rules » across Europe, often fiscal aspects determine the « civilian strategy » to adopt.

It is likely that, for people who may have a choice of law, said choice will be dictated by the desire to obtain the most favorable tax regime, in order to protect their Loved Ones.

This particular issue will be addressed in detail, in a future article.

In the meantime seek the best advice to protect the ones you love, and put your mind at rest.