Author Archives: Edouard Figerou

Trust in France – Part 1

Trust is a widespread institution in foreign legal systems, especially in Anglo-Saxon law, but unknown in French civil law.

However in 2011, France defined trust for tax purposes only.

Trusts are characterised in so much as that property is divided between the legal ownership (‘propriété juridique’ given to the trustee of the trust who becomes the legal owner of the transferred assets) and the equitable interest (i.e virtual property residing in the right or title to assets, property or rights held for the beneficiary by the trustee in whom resides the legal title).

This property split is not to be confused with what we know in France as the ‘demembrement de propriété’ between usufruct and bare ownership.

Quick reminder: The right of ownership gives the owner three types of prerogatives. If we take the example of a property, these prerogatives consist of the right to use the property (i.e. to live in it), the right to receive income from said property (i.e to rent it out), and the right to dispose of the property (i.e. to sell it).

However an owner can divide these prerogatives into two sets: on the one hand what’s called « usufruct » which includes the right to use the property and receive its income, and on the other what’s called the « bare ownership » which includes the right to dispose of the property.

Therefore the right of ownership is the combination of the usufruct and the bare ownership.

In 2011, France defined trust for tax purposes only. Article 792-0 bis of the General Tax Code (Code Général des Impôts) defines trust as all legal relationships created under the law of a State other than France by a person called ‘grantor’ (settlor), inter vivos or mortis causa, in order to place assets or rights under the supervision of a ‘trustee’, in the interest of one or more ‘beneficiaries’ or to achieve a specific goal.

Are therefore considered to be trusts all legal relationships meeting this definition, regardless if they effectively go under the name of ‘trust’ and also regardless of their characteristics (whether revocable or not, discretionary or not, with or without legal personality, etc.).

On the other hand do not meet the definition of article 792-0 bis of the CGI:

- Trusts established by a company or group of companies such as trusts established by companies and dedicated to the management of employee saving schemes or stock option plans.

- Trusts called « unit trusts » that meet the definition of UCITS, Undertakings for Collective Investment in Transferable Securities.

The Grantor/Settlor

Article 792-0 bis of the CGI stipulates that the grantor of a trust is the individual that created it.

This definition allows us to discern the economic reality of a trust whatever its legal appearance or name. In practice, the aim is to determine the ‘real’ settlor of the trust in the event the settlor, sole entity named in the deed of trust, is an entity (….) or an individual acting professionally designated on behalf of the real owner of the assets placed directly or indirectly through one or more corporations, in the trust.

Furthermore the same article foresees taxation of accumulation trusts upon death of the settlor, and then in some cases upon death of the beneficiaries deemed settlors. Said taxation of the assets remaining in the trust takes place upon each change of beneficiary (for example, when the children of the initial beneficiary become replacement beneficiaries upon death of their parents).

The Beneficiary

The tax beneficiary of a trust means the person (one or more) designated to receive the income of the trust made by the administrator (trustee) and/or to receive the capital value of the property or rights of the trust during the life of the trust or at its end.

This definition does not exclude the grantor from also being a beneficiary of the trust, especially in the situation of an ‘inter vivos trust’.

In part 2 we will address trust and estate planning here in France.

French & UK Capital Gains Tax & Social charges

What to know about double taxation…

The French & UK Tax treatment of capital gains & social charges

On the sale of a French property:

Gains made from the sale of a property situated in France are liable for French Capital Gains Tax (CGT) + French ‘prélèvements sociaux’.

Therefore a UK resident selling a property situated in France will be subject to French CGT & social charges. But equally and due to the fact he/she is a UK resident, he/she will also be subject to UK Capital Gains Tax on the same sale.

On the sale of an English property:

Gains made from the sale of a property situated in the UK are liable for UK Capital Gains Tax. No English equivalent of ‘prélèvements sociaux’ are due.

Therefore a French resident selling a property situated in the UK will also in theory be subject to English CGT. But he/she will equally be subject to French Capital Gains Tax & ‘prélèvements sociaux’ because he/she is a French resident.

=> In effect we are potentially looking at taxation on both sides of the Channel, and that’s where the double tax treaty comes into play.

Double Tax Treaty (DTT) or Double Taxation Convention (DTC)

A double tax treaty was signed between France & the UK for corporation tax, income tax and capital gains on June 19th 2008.

The purpose of the Double Tax Treaty is not to allow the taxpayer to choose in which country he/she would rather pay tax, nor does it elect in which country (either the UK or France) tax should be paid – but it simply allows that:

– for a UK resident, any French tax paid will be credited against the UK tax arising from the same gain,

– & vice-versa, for a French resident, any UK tax paid will be credited against French tax arising from the same gain.

Let’s take a more detailed look at the possible situations:

I./ Residents

French taxpayers such as British nationals residing in France

On the sale of a French property by a French resident basic French rules of taxation, rates, main exemptions and taper relief apply.

On the sale of a French property by a French resident basic French rules of taxation, rates, main exemptions and taper relief apply.

On the sale of a UK situated property by a French resident we will need to make a distinction between two cases: whether tax was, or not effectively paid in the UK.

On the sale of a UK situated property by a French resident we will need to make a distinction between two cases: whether tax was, or not effectively paid in the UK.

I./1 If no tax was effectively paid in the UK on the sale of a UK property

As a result of the new Franco-British DTT no tax credit can be granted in France and the gain is taxable under French law.

Therefore French Capital Gains Tax and social charges are due on an English gain.

How to declare & pay said gain?

In practice a certain amount of forms will need to be filed out:

– One specific form that must be filed at the local tax office within two months following the sale, accompanied by the corresponding payment of the tax.

You may ask your notaire or accountant to help you with this procedure.

– And two general tax returns to report the gain. The aim is to take said gain into account when determining the general tax rate of the household for that year.

I./2 If tax was effectively paid in the UK on the sale of a UK property

Principal of elimination of double taxation

In contrast to the situation we have just seen above, here the gain actually supported tax in the UK, therefore France (State of residence) will apply rules to eliminate the double taxation, with a system of tax credit.

The vendor will be entitled to a tax credit against French tax, equal to the amount of the foreign tax paid. However such credit shall not exceed the amount of French tax attributable to such income. Therefore if the foreign tax exceeds the French tax no deduction on the global tax due by the household will be granted and no refund will not be achieved.

II./ Non-Residents

British nationals residing in the UK selling a property in France

On the sale of a French property by a non-resident basic French rules of taxation and rates, main exemptions and taper relief apply.

However capital gains made on an occasional basis by taxpayers domiciled outside France are subject to some French specificities.

- French tax is due & some specific measures will apply

– ‘Prélèvements sociaux’

Since August 2012, non-residents have been made liable for the social charges, where previously they were merely liable for the main capital gains tax.

Therefore the basic gross tax rate for residents of France and the European Economic Area (EEA) residents is 34.5%, whilst for those from outside the EEA it is 48.8%.

In the same manner as capital gains tax, tapered relief is granted on social charges but over a longer period of 30 years (against 22 years for CGT).

What are social charges?

‘Prélèvements sociaux’, also known as the ‘contributions sociales’, actually comprises 5 different taxes. They do not all generate an entitlement to social security benefits, therefore it is incorrect to say that said charges are social security contributions.

However several court cases are currently pending before the Court of Justice of the European Union because the application of said charges to non-residents is deemed unjust, and contrary to the EU principal of free movement.

France faces a bill of 344 million euros for 2012.

– Représentation accréditée

Non-resident individuals subject to French CGT must under certain circumstances appoint a tax representative who will be jointly liable on said tax until its prescription date.

If the tax representative is a legal entity they charge for their intervention.

This measure is also under the spotlight of Europe.

Portugal was condemned by the European court in 2011. In anticipation of a French condemnation the French amending Budget Act for 2014 proposes to remove the requirement for EU resident taxpayers.

- UK CGT may also be due

So we have seen that if you are a non-resident selling a property in France you will be subject, for the moment to French CGT & social charges.

But that is not all you will be subject to: UK CGT may also be due.

I will not go into the basics of UK CGT here that is not the aim of this article. More importantly let’s look at what the double tax treaty states.

Following the sale of a French property the treaty’s provisions allow for the French tax already paid to be offset against the UK tax. If the French tax is greater no deduction against similar tax is granted in the UK. In such a case, there would simply would be no tax to pay in the UK.

Note: The amount of French tax paid can only be taking into for the CGT part and not the ‘prélèvements sociaux’ part. HMRC has a clear position when it comes to French ‘prélèvements sociaux’: they are not considered as ‘tax’, therefore they are excluded from the charges for which credit is allowed against UK capital gains tax.

If you are affected by any of the situations mentioned above – be it a French resident selling a property in the UK, or a UK resident selling a property in France – you may need to be more vigilant when it comes to your tax obligations.

Les notaires sur Tv7

La Chambre des notaires de la Gironde diffuse, une semaine par mois, sur TV7 une émission appelée « Solution notaire» durant laquelle un notaire aborde tous les aspects d’un thème particulier.

Inheritance planning New inheritance rules under EU Regulation of July 4th 2012

… or potentially, the key to put your mind at rest

For those of you with international profiles – living abroad, or who own assets abroad – new EU measures represent a major step forward for your estate planning.

And this will apply from August 17th, 2015.

Under current French inheritance law

French inheritance laws are very different from those of the United Kingdom.

In France you are not free to dispose of your whole estate as you may wish.

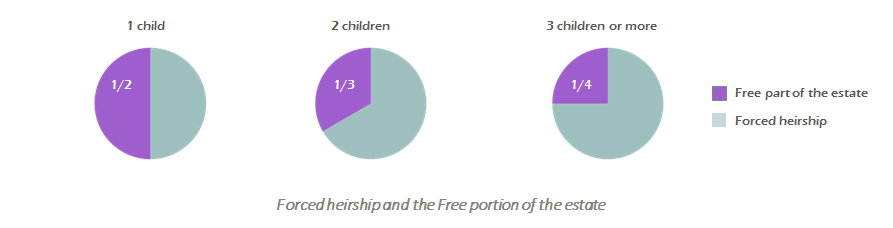

Upon death the deceased’s estate is divided into two sections, called:

- « la réserve héréditaire », or what’s known as « forced heirship »– which must be left to any protected heirs, i.e your children

- and « la quotité disponible », which represents the free part of your estate, which can be left to whoever you wish.

If you have children, and whether you draft a will or not, you cannot disinherit your children. They are legally entitled to a share in your estate:

- If you leave 1 child, he/she is entitled to 1/2 of the estate,

- If you leave 2 children, they are entitled to 1/3 of the estate each,

- If you leave 3 or more children they are entitled to 3/4 of the estate in equal shares.

You may have already taken measures to mitigate French inheritance rules, you may have:

- changed your marital regime,

- created an SCI,

- bought in tontine,

- put in place a gift between spouses, etc.

Whether you have taken measures or not, your situation will need to be reviewed in light of the new EU regulation.

« Forced heirship » rules will not disappear, but from August 2015 it will be possible for some of you to dispose freely of your whole estate.

New inheritance rules under EU regulation n°650/2012

From August 17th 2015:

- If the deceased says nothing in his/her will, or in the absence of a Will, his/her last habitual residence at the time of death will determine the laws of his/her succession.

- However, the testator is allowed to designate his/her national law (at the time of the choice or the time of death) as the law governing his/her succession as a whole, by stating his/her choice expressly and in testamentary form.

For example an English citizen can choose English law to govern his/her succession as a whole, by stating so in a will.

The context of these rules

The purpose of Brussels IV is to facilitate free movement, within the EU, by removing the obstacles faced by EU citizens in asserting their rights in the context where the deceased’s assets are situated in different countries.

In particular it provides certainty as to which law will apply in governing your succession.

The regulation is of universal application

Whether it be the law of the country of habitual residence or the law of the testator’s nationality, said law will govern the succession as a whole, including all worldwide assets, regardless of their nature (movable or immovable assets), and their location (whether they are located in another EU State or a state outside the EU).

When does it come into effect?

The regulation:

- came into effect on August 16th 2012,

- but will only apply from August 17th 2015.

In practice this means that you can already prepare your inheritance in accordance to said regulation, by writing your will now, however it will only apply if you live until August 17th 2015.

What can this mean for you?

It will facilitate your estate planning

Because not only will you be able to choose the law applicable to your inheritance; but said law will govern the whole of your worldwide assets.

It will enable you to mitigate side effects of the law of habitual residence

If the law of your habitual residence doesn’t permit you to dispose of your estate how you wish, you may choose your national law to achieve your aim.

For example if you are an English national living in France, you can choose English law and therefore avoid the French « forced heirship » rules, enabling you to dispose freely of your entire estate.

Exit some old strategies, like creating an SCI to avoid French inheritance rules. A simple Will may suffice.

A sole and unique law governing the whole of your succession will simplify international inheritances considerably.

However every clients situation is different and needs careful analysis and even though these new rules will open up great new perspectives, their application will not be plain sailing – seek the best advice to protect the ones you love, and put your mind at rest.

Some foreseeable difficulties

The UK, Ireland and Denmark have opted-out of EU Regulation n°650/2012

In practice this will have a strange effect:

- UK citizens living abroad will be able to benefit from these rules,

- Whereas other EU citizens (French nationals, for example) living in the UK will not, because the UK does not abide by the regulation.

So if said French national, living in the UK has property in the UK, he cannot chose for said property to be dealt with under French law.

The concept of Habitual residence adopted by the EU has not been defined

It may reveal difficult to prove; and the lack of definition leaves room for manipulation.

If we take the example of the UK, UK’s internal private law is coordinated around the concept of « domicile ».

Said notion is complex and involves numerous aspects, encompassing habitual residence, place of birth and centre of economic interests, etc…

In English law an English national may have lived a large part of his life outside of the United Kingdom and still be regarded as « domiciled’ in his country of origin if he/she intends to return.

In practice, we may be confronted with situations whereas:

- An English lawyer will consider the deceased domiciled in England and apply English law, and a French notary who will consider the deceased to have his habitual residence in France, and apply French law to the whole of the deceased’s estate.

Therefore it is essential to explicitly choose the law that will govern your future inheritance in a will.

- Acceptance and application of EU Regulation in a third member State

- Other issues concern the domains excluded by the Regulation, such as:

- Matrimonial regimes…

- Gifts …

- Tax issues

These will remain governed by the state in which the assets are held and double tax treaties between the states is they exist.

Because of the disparities in « tax rules » across Europe, often fiscal aspects determine the « civilian strategy » to adopt.

It is likely that, for people who may have a choice of law, said choice will be dictated by the desire to obtain the most favorable tax regime, in order to protect their Loved Ones.

This particular issue will be addressed in detail, in a future article.

In the meantime seek the best advice to protect the ones you love, and put your mind at rest.